Voices shaping knowledge through insight

Op-Ed

12

Apr

- April 12, 2026

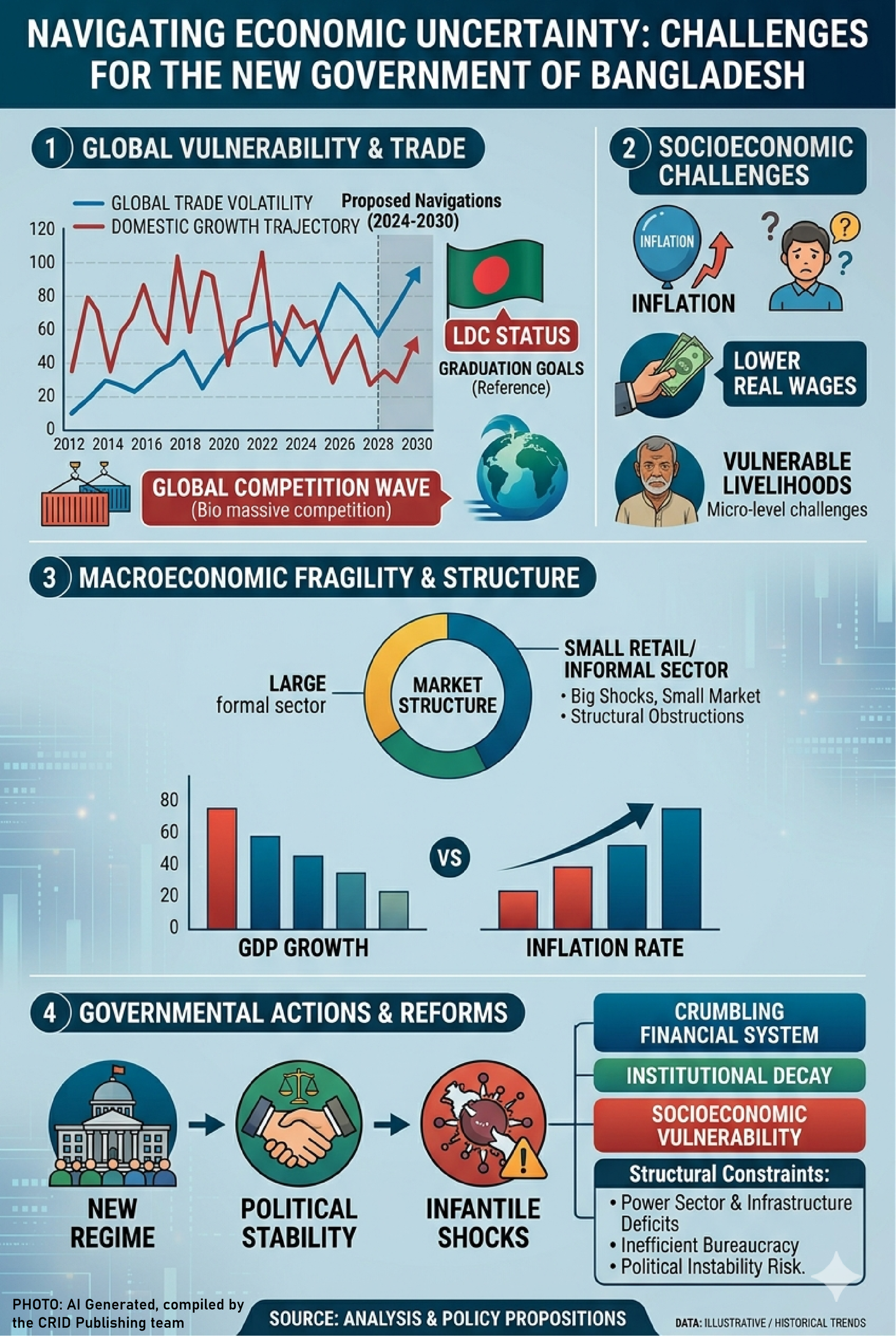

Navigating Economic Uncertainty: Challenges for the New Government of Bangladesh

By Md. Hasinur Rahman and Aritro Roddur Dhar

Despite a transition toward political stability, Bangladesh continues to struggle with high inflation and a crumbling financial infrastructure that undermines its macroeconomic goals.

The economy of Bangladesh has been under a complicated transition, and the country has been experiencing low GDP growth, incessant inflation, and a crumbling financial system in recent times. Although the assumption of power by the Bangladesh Nationalist Party through a peaceful, fair election has had the effect of providing a possible path to political stability, the new regime is faced with a weak macroeconomic environment that is typified by structural obstructions and infantile shocks. The strategic change that has been most eminent and has been made by the new cabinet is the alarming request to delay the graduation of Bangladesh as a Least Developed Country (LDC) to the year 2029. This move reflects a sobering realization: while the “macro” numbers once promised a smooth exit, the “micro” reality of institutional decay and socioeconomic vulnerability suggests the nation is not yet ready to face the global market without its LDC safety net.

Macroeconomic Fragility and Structural Constraints in Contemporary Bangladesh:

The impacts of air pollution on climate change in Bangladesh are multifaceted. Air pollutants such as black carbon (BC) and other short-lived climate pollutants (SLCPs) have a significant warming effect on the atmosphere, leading to the accelerated melting of Himalayan glaciers, rising sea levels, and extreme weather events. These impacts have severe implications for Bangladesh, a low-lying deltaic country, which is already vulnerable to the effects of climate change. Moreover, climate change can exacerbate air pollution by increasing the frequency and severity of weather events, leading to more forest fires, dust storms, and air pollution.

The current economic situation in Bangladesh can be characterized by a continuous attempt to maintain sustainable economic growth in the face of long-term instability. The narrative of resilience has prevailed over the decades, but in fiscal year 2025–26 this resilience is being pushed to the extreme.

Growth Slump and Investment Paralysis: The GDP growth has been very slow, with 3.97% growth per annum in FY2025 compared to 4.22% growth in the previous year.

The overall FY2026 projections expect a very slight recovery of about 5.1; however, this will only be possible in the event of total political calmness. The engine of this growth – private investment is currently paralyzed. Major investment indicators have shown a significant decline, reflecting an environment constrained by high financing costs, energy shortages, and weak contract enforcement. Despite the interim government’s efforts to attract FDI, there has been little improvement in the situation.

The Inflationary Trap: Inflation has become the most visible symptom of Bangladesh’s economic distress. Headline inflation is stuck at 8.58% (January 2026), with food inflation rocketing to 8.29%. Despite the central bank raised the repo rate 11 times since May 2022, the effect is still negligible. This fact implies that inflation in Bangladesh is no longer just a monetary phenomenon; it is driven by supply-side bottlenecks, market hoarding, and high intermediational margins where middlemen inflate prices of perishables before they reach the consumer.

The Debt and Fiscal Chasm: The current fiscal landscape is increasingly claustrophobic. Public debt has exploded, surpassing Tk 21.44 trillion as of June 2025, a 13.5% year-on-year increase. To meet annual revenue targets, the government requires a phenomenal 32.8% growth in revenue collection for the remainder of FY2026, a feat nearly impossible without radical changes in the tax collection system.

Immediate Stabilization Priorities and Policy Trade-offs Facing a Prospective BNP Administration:

The new leadership is facing a trial by fire, where the most urgent issue that it is trying to solve is the LDC graduation deadline that initially was due in November 2026. The Economic Relations Division (ERD) has officially requested the United Nations Committee on Development Policy (CDP) to further extend the preparatory period up to November 24, 2029. The government claims that the world and national shocks of the pandemic, the war in Ukraine and Russia, and recent domestic unrest are disrupting the national “Smooth Transition Strategy.”

Technically, Bangladesh still meets the three graduation criteria:

- Per Capita GNI: Remains above the threshold.

- Human Asset Index (HAI): Shows continued progress in health and education.

- Economic Vulnerability Index (EVI): Though improved, it hides the weakness of the RMG-dependent export model.

The challenge is empirical: the government must convince the UN that the socio-economic situation has deteriorated so severely that graduation would trigger a reversal of development. Failure to secure this deferral would mean the immediate loss of duty-free access to the EU and other markets, potentially squeezing RMG profit margins by 5–10% and risking the jobs of millions.

Proposed Institutional Remedies:

- Monetary-Fiscal-Market Coordination: The current “coordination deficit” must be closed by empowering a central body to align the central bank’s interest rate hikes with the Ministry of Commerce’s supply-chain monitoring.

- Central Bank Autonomy: The Bangladesh Bank must be shielded from the “political considerations” that have historically led to the granting of new bank licenses to party loyalists.

- NBR Modernization: Expanding the tax base is no longer optional. The government must move beyond its reliance on import duties and VAT, which disproportionately affect the poor, and implement a robust direct tax system that targets high-net-worth evasion.

Assessing Governing Capacity: Institutional Pragmatism versus Populist Macroeconomic Management

Bangladesh’s economic woes are, at their core, a failure of institutions. The “institutional failure” is not a single event but a systemic sclerosis that has hollowed out the state’s regulatory capacity. The banking sector is currently in its most precarious state in three decades. Profitability indicators are in the red: Return on Assets (ROA) fell to -0.58% and Return on Equity (ROE) plummeted to -16.11% in 2025. These are the lowest figures in nearly 30 years. The root cause is a combination of deteriorating asset quality (Non-Performing Loans) and high provisioning requirements. For years, “family-dominated boards” and political interference allowed for reckless lending, leaving the banking system a shell of its former self. In our case, political stability must be viewed as an economic asset. Without a clear “election roadmap” and the restoration of law and order, particularly in the industrial belts of Ashulia and Gazipur, FDI will remain elusive. The government needs to foster a “conflict-free environment” through stakeholder dialogues, ensuring that RMG labor disputes are settled through global standards rather than coercion. The question of whether the BNP administration is capable of steering this ship remains under heavy scrutiny. While the government inherits a significant “honeymoon” period, its early actions suggest a tension between technical pragmatism and political survival. The Finance Ministry, under Amir Khosru Mahmud Chowdhury, has shown a willingness to stocktake resources, but inter-ministerial synergy remains weak. In past regimes, the disconnect between the Ministries of Energy, Finance, and Commerce often led to policy paralysis. If the current government cannot synchronize fuel price adjustments with transport subsidies and inflation targets, the “capability” of the cabinet will be called into question. The true measure of capability will be the government’s resolve against its own supporters. For decades, “crony capitalism” has been the bedrock of political funding in Bangladesh. Can the BNP-led government crack down on the “business syndicates” that hoard essential commodities, even if those syndicates have ties to the party? Deep scrutiny suggests that unless the government implements an Independent Anti-Corruption Commission with real prosecutorial teeth, the structural fixes will remain superficial. Simultaneously, the government must manage a $4.55 billion IMF program. The IMF demands fiscal discipline, yet the BNP administration faces immense pressure to deliver on populist promises, such as a proposed Tk 1 trillion civil service pay hike. Balancing these competing demands without triggering a sovereign debt crisis or hyperinflation is the government’s most immediate hurdle. The LDC deferral request is a test of diplomatic capability. The government is drawing on precedents like the Solomon Islands (deferred due to civil unrest) and Nepal (deferred due to the 2015 earthquake). However, unlike those nations, Bangladesh’s macro-indicators still look “too good” on paper for an easy deferral. The government’s ability to present a data-driven case of “hidden vulnerability” will determine the country’s trade fate for the next decade.

Historical Political Economy of the BNP: Economic Governance, Reform Trajectories, and Developmental Outcomes

To predict the future, we must analyze the BNP’s past performance, which offers a study in both visionary reform and systemic decay. During the 1991-1996 term under Khaleda Zia, the administration spearheaded the most significant liberalizing reforms in the nation’s history. This era was defined by a fundamental shift away from aid dependency toward a market-oriented economy. The legislative landmark of the VAT Act of 1991 did more than merely streamline revenue; it fundamentally re-engineered the fiscal architecture of the state. Simultaneously, the Financial Sector Reform Programme (FSRP) and the Bank Company Act of 1991 introduced the first semblance of prudential regulation and uniform accounting to a nascent banking sector. Perhaps most critically, the 1991 Industrial Policy, which allowed for 100% foreign ownership, acted as the primary catalyst for the Ready-Made Garment (RMG) revolution. In those five years, GDP growth averaged 4-5%, and the country successfully shed its “bottomless basket” image. However, the 2001-2006 tenure presents a far more complex and cautionary narrative. On a purely macroeconomic level, the government achieved impressive results, with annual growth accelerating to 5-6% and foreign aid reliance falling to a record low of 2% of GDP. The successful management of an IMF Poverty Reduction and Growth Facility (PRGF) helped stabilize reserves, which later hit $45 billion before the current crisis. Yet, these gains were severely undermined by profound institutional and governance failures. This period is historically remembered for Bangladesh ranking at the bottom of Transparency International’s Corruption Perception Index for five consecutive years. This pervasive corruption created a high-cost economy that stifled long-term potential. Even more damaging was the failure to invest in the power sector. A lack of new generation capacity led to chronic “load-shedding” that crippled Small and Medium Enterprises (SMEs) and forced subsequent regimes into expensive and corruption-prone “quick rental” power solutions. The energy insecurity born in the mid-2000s remains a structural bottleneck today. As the current BNP-led government pushes for a 2029 LDC deferral, it is essentially asking for time to reclaim the reformist spirit of 1991 while attempting to prove it has learned from the governance failures of 2001. Success this time will require more than just liberalization; it will require the moral and political courage to dismantle the very “crony” structures that the party itself has been accused of fostering in the past. The “return” of the BNP today is built on a rhetoric of “structural fixes” and “national agenda”. They are drawing on their 1991 legacy of liberalization to argue for the 2029 LDC deferral, claiming they need time to repeat that early success. However, the 2001 legacy of corruption and power sector neglect serves as a warning. Success in 2026 will require the 1991 spirit of bold reform without the 2001 trap of institutional decay.

Bangladesh is at a critical juncture. The path to 2029 is not merely about delaying a graduation ceremony; it is about rebuilding the very foundations of the state. The government’s capability will be judged not by its rhetoric, but by its ability to turn the LDC deferral into a “window of reform” rather than a “stay of execution.” To navigate this uncertainty, the nation requires a rare fusion of academic policy-making and human-centric governance, one where the macro-stability of the state finally translates into the micro-security of its citizens.

Authors’ Information

Md. Hasinur Rahman, Research Assistant, CRID, Dhaka, Bangladesh

and Aritro Roddur Dhar, Research Intern, CRID, Dhaka, Bangladesh

Note: All opinions, and any matters relating to plagiarism or copyright, are the sole responsibility of the author(s) and do not reflect the position of Centre for Research and Information (CRID)